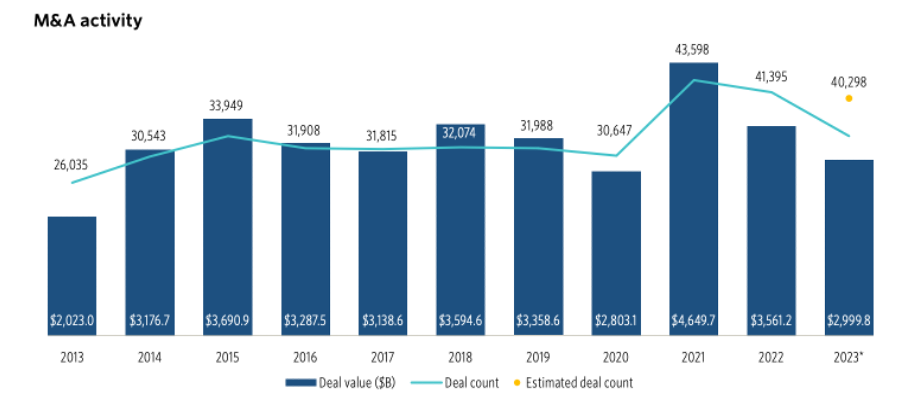

The Global M&A market

After deal value peaked in 2021 and then plummeted in the wake of the pandemic, dealmaking in M&A revived in 2023, with pharma companies pursuing revenue growth and MedTech companies chasing profitability.1 Over 2023, it reaches considerable deal amounts across the life science sector.

Overview data from Pitchbook show us that the highest M&A activity in terms of both deal value and deal count occurred in 2021. After that, both metrics show a decline, indicating a slowdown in M&A activity, with the estimated values for 2023 continuing this downward trend. Deal value declined to $2999 billion in total in 2023, reaching the lowest value since 2020.2

Figure 1 Global M&A activity

Figure 1 Global M&A activity

The primary driver was the pandemic: consumer activity was sluggish, and an economic recession became increasingly evident, leading to a rise in bank interest rates, which is the most direct reason in driving this stagnant situation. Other reasons include inflation caused by the higher interest rates, which created a vicious cycle for both individual consumers and companies, resulting in an even more severe economic downturn.

Due to the continuing recovery from the pandemic, consumer economic activity remains very weak, and many companies across various industries do not have sufficient liquidity to engage in M&A deals, leading to negative growth in global M&A activity from 2022 to 2023. Additionally, many small-scale companies in various sectors have gone bankrupt due to a lack of liquidity to repay short-term loans.

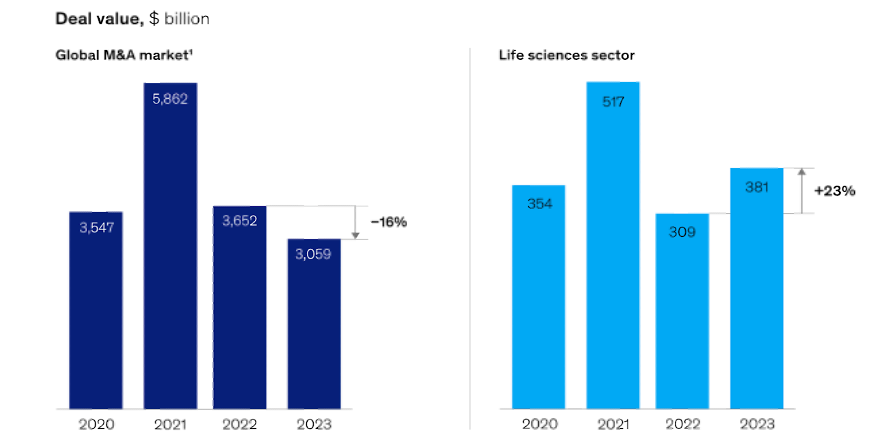

Life Science Dealmaking

Differentiated from the global M&A market, dealmaking in life sciences (including biotech, pharmaceutical, and MedTech) saw an upswing in 2023. The global M&A deal value decreased by 16% from 2022 to 2023, while the life sciences sector’s deal value went up sharply between 2022 and 2023, increasing 23% in total. This was completely contrary to the broader market trend.1

Life sciences M&A transactions were higher in 2023 compared with 2022. Although the year started slowly in January and February, March through June saw steady deal activity, at which point experts began projecting that 2023 could be the biggest M&A year since 2019. The excitement dwindled, however, as the deal market slowed through the rest of the summer, culminating in a nearly dead market by late September. Optimists pointed out that many biotech companies announced that they were exploring “strategic alternatives” in the third quarter, speculating that a new deal surge could be on the horizon.

That speculation proved to be prescient, as there were 27 M&A transactions in the fourth quarter, bringing the 2023 total biopharma M&A upfront to $128.8 billion.3

Figure 2 Comparison between Global and Life Sciences M&A deal value

Figure 2 Comparison between Global and Life Sciences M&A deal value

How does this situation appear? The global pandemic served as an incentive for the life science sector companies to pursue innovation in advanced modalities like mRNA and cell and gene therapy to find a cure, which required considerable assets. Thus, their main target was generating financing for their pipelines, which pushed them to find solutions to accumulate retained earnings while increasing profits to revitalize the entire life science market.

In 2023, large pharmaceutical companies focused on pursuing a series of smaller deals or “bolt-ons” rather than “mega” deals valued over $1 billion. In the first half of 2023, M&A sellers mostly consisted of small-cap public biotech companies and private sellers. The proportion of M&A mega deals declined 56% since 2021’s record high, while M&A deals with values less than $1 billion declined only 20%.3

Small biotechnology companies looked to the financial clout of big pharma companies and private equity (PE) players for R&D and product development support, driving the overall increase in deal value across the biotech and broader life sciences sectors.

Key Drivers behind the Dealmaking Surge in Life Sciences

The main catalyst behind this trend is the life science sector’s focus on a steady stream of small, strategic transactions to fill gaps in their portfolios or to enter new market segments. Instead of pursuing mergers with large companies or entire industrial chains, these smaller deals allow companies to address specific market needs and diversify their offerings more effectively.

Total shareholder return (TSR) analysis is a crucial tool for companies to measure their profitability in the market. Data from some biotech and pharmaceutical companies show that engaging in several small life science transactions tends to result in higher and steadier TSR than making selective or large acquisitions at once. This is in part because they are easier to integrate and less risky. On the other hand, larger acquisitions can lead to higher initial volatility, which will appear in the variance of TSR due to integration risks, financing costs, and initial disruptions before synergies can be realized. Specifically, the programmatic approach works well in the pharmaceutical, biotech and MedTech industries.

For example4, in 2023, Thermo Fisher Scientific, a world leader in science services, announced that it had completed the acquisition of CorEvitas, a company specializing in regulatory-grade real-world evidence solutions, for $912.5 million in cash.

CorEvitas operates across multiple registries, with a focus on in autoimmune and inflammatory diseases. For over 20 years, it has partnered with pharma and biotech customers to provide regulatory-grade, real-world evidence solutions with objective data and clinical insights to improve patient care and clinical outcomes. CorEvitas manages 12 registries, including nine9 autoimmune and inflammatory syndicated registries. Its multi-therapeutic data intelligence platform builds and scales multiple clinical registries across specific therapeutic areas to gather structured patient clinical data spanning more than 400 investigator sites and following over 100,000 patients longitudinally.

According to data from Thermo Fisher, the transaction is expected to be accretive in 2023 and deliver $0.03 of adjusted earnings per share in 2024.4

The current market environment is putting strong financial pressure on the life science companies. Life science like companies, particularly MedTechs, are responding by changing their approach to value creation. Along with the current condition of rising interest rates in global markets, it’s forcing them to focus on improving their margins to secure higher valuations in the capital markets.

1) Reshaping the Portfolio

Life science companies focus more on the weighted average market growth rate of the businesses in their portfolio. They divest slow-growing, less profitable assets but target at growth-oriented acquisitions in pursuit of higher aggregate growth to improve their financial profile.

One example is Medtronic, which restructured its portfolio by divesting its patient monitoring and respiratory interventions businesses to raise cash and focus on higher-growth areas like diabetes management and robotics. At the same time, the company has been expanding to high-revenue areas, such as digital surgery and AI-driven healthcare solutions, to enhance its market position.

MedTech company Baxter also adopted a portfolio reshaping strategy in 2023, divesting slow-growing assets and focusing more on expanding high-margin businesses like advanced surgery, biopharma solutions, and renal care.5

2) Taking Advantage of More Transaction Structures

PE firms and certain hedge funds are increasingly offering capital to MedTech companies. These firms often invest in opportunities that may not align with the immediate strategic priorities of MedTech businesses but are aware that many MedTech companies have more potential investment avenues than available funds. As a result, they are approaching these companies to provide financial support.

At the same time, many potential buyers are exploring alternative deal structures. Joint ventures are becoming more prevalent in MedTech. Companies are establishing long-term strategic collaborations with digital firms, co-investing with PE firms, and securing external funding to support R&D efforts, with product royalties as part of the compensation.

Outlook:Life Science M&A for 2024

According to this report, there are three key reasons to expect the rising trend in M&A spending to continue and accelerate in 2024 and beyond: the biopharma industry still holds near-record levels of M&A firepower6; the industry faces major revenue challenges in the next five years and needs to secure inorganic growth6; and economic conditions mean there is a buyer’s market favoring acquiring companies.

Despite its increased M&A investment, the industry still commands more than $1.37 trillion6 in dealmaking capacity.

In the upcoming series of articles, we will delve into the details, focusing on the financial metrics of each sector within life sciences, and examine whether the M&A deal value in 2024 aligns with the optimistic predictions. Stay tuned for more in the next article!

References

Bernauer, Torsten, Rebecca Kaetzler, Rajesh Parekh, and Jeff Rudnicki. “Life sciences M&A shows new signs of life.” McKinsey & Company. 29 Feb. 2024.

Global M&A Report. Pitchbook 2024.

“Life Sciences 2024 Dealmaking Trends & Outlook.” Ropes & Gray. 4. Mar. 2024.

Thermo Fisher Scientific Completes Acquisition of CorEvitas. Thermo Fisher Scientific. 14 Aug. 2023.

“Medtronic, Baxter face FDA Class I labels for separate recalls of heart pumps, ventilators.” Fierce Biotech. 23 Jun. 2022.

“2023 Global Life Sciences Outlook.” Deloitte. Accessed 1 Oct. 2024.