Why Biosimilars?

Recombinant proteins, antibodies, and other types of biologic drugs were first introduced several decades ago and offered a new approach to the treatment of disease quite different from that of small molecule drugs. In the intervening years, they have slowly accounted for greater percentages of approved products and pipeline candidates. However, biologic drugs are quite expensive.

Not surprisingly, the desire to offer generic versions of biologic drugs arose as a means to reduce costs to payers and patients. Unlike small molecule drugs, which have specific molecular formulas and structures for which it is possible to chemically synthesize identical copies, biologics are produced using living cells. Variations in structure and molecular composition can vary slightly from one manufacturing batch to another, and consequently there is no definitive structure and mechanism for producing identical copies.

Biosimilars have become the industry’s solution. They are similar to the original, branded reference product in structure and other characteristics (e.g., purity, bioactivity) as proven through comprehensive characterization methods and shown to have no clinically meaningful differences in terms of safety and effectiveness.1,2

The development of biosimilars is much more complex than that for generic drugs in terms of time, effort, and costs. Bioprocesses are more complicated, demonstration of comparability requires extensive analytical work, and clinical trials must be conducted. As a result, while generic drugs often are sold at a small fraction of the price of their branded counterparts, the maximum savings for biosimilars compared to their reference products is typically 15–30%. Even so, given the high prices for these drugs, the savings potential is significant.

To date, biosimilars have been developed for many types of recombinant proteins and monoclonal antibodies to treat a wide array of conditions, including cardiovascular and autoimmune diseases, blood, metabolic, and rare genetic disorders, and cancer, among others.3,4

Marketed Since 2006

The first marketing authorization for a biosimilar was granted to Sandoz’s Omnitrope, a biosimilar of Pfizer's Genotropin (somatropin (rDNA origin)) in 2006. A first attempt by Sandoz to gain approval using the “well‐established medicinal use” route” was rejected by the European Commission in 2003 despite its recommendation for marketing authorization by the Committee for Medicinal Products for Human Use of the European Medicines Agency (EMA).3 Approval was obtained in 2006 only after a framework specifically for biosimilar approval was implemented. Approval for this same biosimilar was also granted in Japan in 2009.

The first monoclonal antibody (mAb) biosimilar (Remsima/Inflectra (infliximab) from Celltrion and Hospira for infliximab) was approved by the EMA in 2014, This approval was also notable for addressing the same range of autoimmune diseases approved for the branded product (known as an indication extrapolation).

It was not until 2015 that the 2014, first approval for a biosimilar occurred in the United States (for Zarxio (filgrastim) from Sandoz).

Table 1 presents biosimilar approval information for selected markets (Australia, Canada, the European Union, the United Kingdom, and the United States.5 Note that only biosimilars approved under the U.S. FDA’s biosimilar pathway are included in the U.S. data.

Table 1. Biosimilar approvals as of May 31, 2024 in Selected Markets5

The number of annual biosimilar approvals has been trending upward in recent years, except for a brief slowdown during the COVID-19 pandemic.

The number of annual biosimilar approvals has been trending upward in recent years, except for a brief slowdown during the COVID-19 pandemic.

Europe Continues to Lead the Way

Europe was not only the first jurisdiction to approve a biosimilar but also the first to establish and build on a strong regulatory approval pathway. The region continues to lead the market with the largest number of approved biosimilars and the widest range of biosimilar products.6 Some of these products have more than 50% market share.6 As of February 2024, a total of 86 biosimilars based on 16 different biomolecules were available on the European market and offering on average a cost savings of approximately 30% compared with their reference products.4

The United States is Catching Up

The United States was initially much slower to approve biosimilar products. While a pathway was theoretically introduced in 2010 through the Biologics Price Competition and Innovation Act (BPCIA),7 effective guidance from the FDA was lacking until 2015. Meanwhile, extensive patent litigation by branded manufacturers has hindered product launches, even for biosimilars with marketing authorization.

Recent years have seen significant positive movement, however. The Inflation Reduction Act (IRA) of 2022, for instance, established incentives for adoption of biosimilars and generics.6 According to one source, by January 2024, 45 biosimilars had received approval, and 38 of them were on the market.8 Another source puts those numbers higher at 61 and 42, respectively, as of early November 2024.9

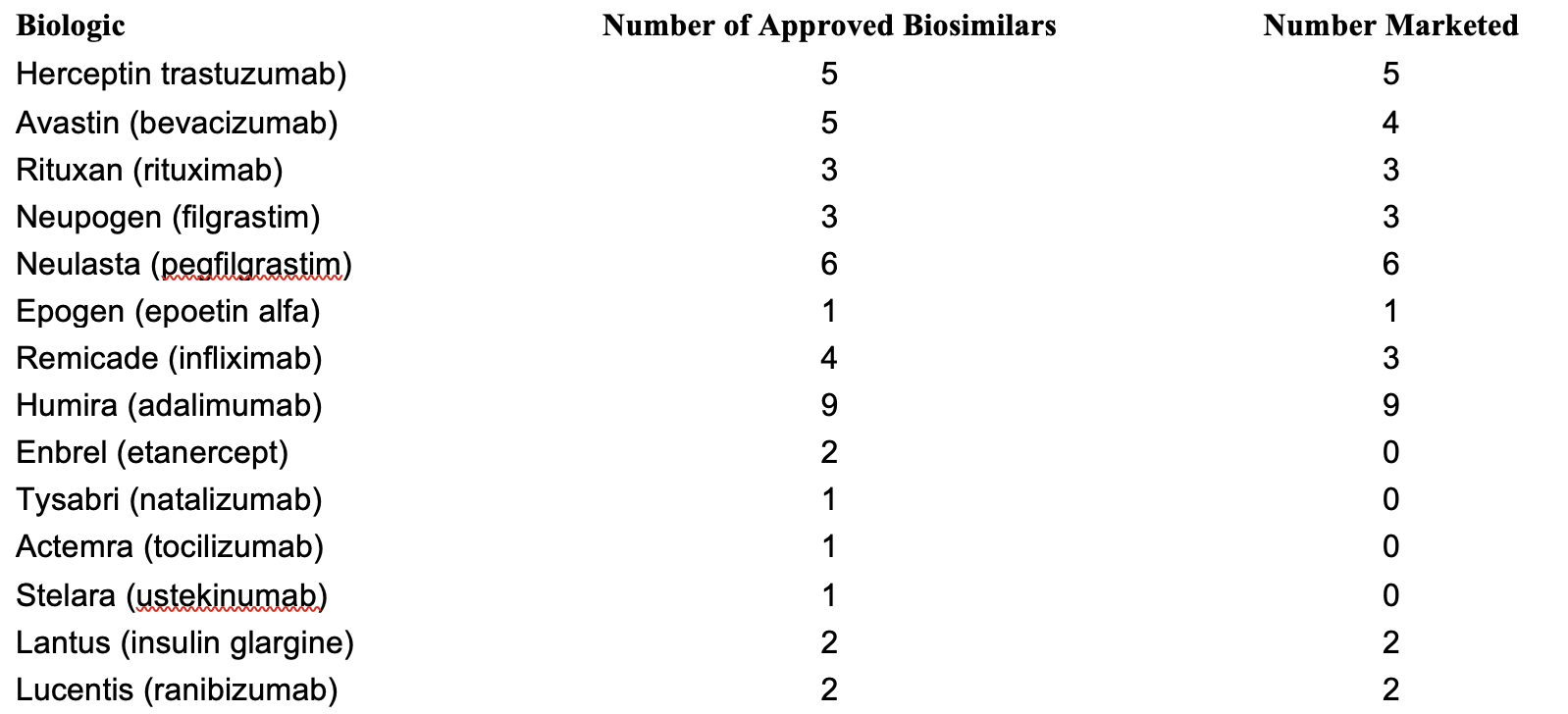

Notably, most of the biosimilars approved in the United States have been developed by large pharmaceutical companies. In fact, there is a separate approval process for manufactures of branded reference products seeking to retain market share through launch of “authorized biologics,” essentially biosimilars, of their own products.

Table 2. Biosimilars approved in the United States as of January 2024 for different biologics8

Significant Activity in Asia-Pacific

Significant Activity in Asia-Pacific

Significant growth of biosimilar markets is also occurring in countries in Asia-Pacific.6 China, India, and Japan comprise the largest biopharmaceutical markets, although South Korea is also an important player in biosimilars.10 Japan, China, South Korea, and Australia all have established biosimilar approval pathways. India issued a guideline in 2012, but as yet has no legal requirements.

Real Progress in Most Other Regions

Outside of these regions, several other countries have mature biosimilar approval pathways, while others have proposed regulations and are working towards established legal requirements, often modeling their systems after either the U.S. or European approaches.10 In North America, Canada and Mexico both have established regulations regarding biosimilars/biocomparables. Most countries in Latin America are not as advanced. Argentina and Brazil have strong regulations, but many others allow marketing of non-comparables, biocopies, biomimics, and non-regulated biosimilars because they still lack internationally recognized regulatory frameworks. Similarly, only a few countries in the Middle East and Africa have established biosimilar approval mechanisms, although many have some basic guidelines or provisions in place.

Many Challenges Ahead

In addition to the complexity of biosimilar development and manufacturing, which act as a barrier to entry for companies seeking to enter the biosimilar market, there are several other factors influencing the rate of biosimilar approvals and launches and general acceptance and adoption. Biosimilar commercialization requires knowledge of bioprocessing, the deep analytical expertise needed to demonstrate comparability, the capability to conduct clinical trials, and understanding of the regulatory landscape.3 Familiarity with pricing policies and reimbursement rates in various markets is also essential.

A further factor is resistance to biosimilars by both physicians and patients. A dearth of knowledge and understanding about the biosimilar approval process initially led both groups to incorrectly associate cheaper biosimilars with lower quality and safety. Education of patients and healthcare providers has slowly begun to have a positive impact. Even so, acceptance of biosimilars is often greater with newly diagnosed patients compared with patients who are already taking a branded biologic drug.10

Variable Adoption Rates

Indeed, acceptance of biosimilars varies greatly depending on the branded biologic and the target market. For instance, in the United States, after three years on the market, the biosimilar for insulin lispro had just 8% market share, while biosimilars for bevacizumab accounted for 82% of the market. Biosimilars of Humira (adalimumab), meanwhile, only held 2% market share by the end of 2023, most likely due to introduction of a more patient-friendly, citrate-free, higher-dosage formulation by AbbVie and special incentives it offered to insurers.11 According to one study, oncology and ophthalmology biosimilars have exhibited fast uptake speeds, while immunology, insulin, and hormone biosimilars have generally demonstrated slower uptake.8

With respect to market differences, adoptions of biosimilars appears to be higher in Europe and the UK compared to that observed in Australia, Canada, and the United States.5 Proposed reasons for the differences include governmental policies, including approval requirements and patent exclusivity laws; reimbursement practices by private and public insurers; rebate policies of pharmacy benefit managers; and laws related to biosimilar substitution (interchangeability).

Need for Global Harmonization

Differences in regulatory approval pathways present another important issue inhibiting development of biosimilars and their distribution on a global basis. Variations exist in different jurisdictions with respect to biosimilar testing requirements, availability of indication extrapolation, length and types of patent exclusivities, and laws regulating interchangeability of biosimilars with their reference products and other biosimilars.5 Even the naming of biosimilars varies. As an example, the World Health Organization has issued its own guidelines using the phrase “biological products that are highly similar” to well-characterized reference products.

Different approaches to issuance of regulatory guidance can lead to variations as well.10 For instance, to obtain approval across the full breath of indications granted to a branded biologic, some authorities require clinical testing for all indications, while others do not. MHRA in the UK automatically allows indication extrapolation, while the EMA, the U.S. FDA, and several other agencies provide specific requirements regarding the evidence that must be provided to support indication extrapolation.

Laws regarding interchangeability can also have a big impact on the use of biosimilars, as some allow pharmacists to fill a prescription with a biosimilar automatically rather than a branded biologic, while others prohibit such activity.12 This issue is of particular importance in the United States, where individual states regulate biosimilar substitution. In most states, a biosimilar must be approved with an interchangeability designation in order for pharmacists to be able to automatically substitute it for the reference product. In Europe, meanwhile, all approved biosimilars are considered to be interchangeable with their reference products or other biosimilars of the same reference product.

There is clearly a need to standardize regulations for biosimilars, starting with basic terminology and including analytical testing requirements to provide comparability/similarity, expectations for clinical testing, indication extrapolation, and interchangeability.

Despite Challenges, Real Cost Savings Realized

Branded biologic drugs can cost as much as $10,000–30,000 per year. With price reductions of 15–35% or more, biosimilars offer potential for significant savings for both patients and healthcare systems.6 In the United States alone, it is estimated that as much as $124 billion in savings could be realized from 2021 to 2025. Another study suggests that over the first 10 years that biosimilars will have been on the market in the United States, total savings could reach $250 billion.7

Rapidly Growing Market

Despite the challenges to bringing new biosimilars to market and the slower adoption rates observed for many of the initially launched biosimilars, growth projects going forward are strong. Such expectations are based on a surge in patent expirations for leading biologic drugs, the increased rate of biosimilar approvals in both Europe and the United States; the increasing maturity of biosimilar regulations around the world, which are leading to increased availability of these cost-effective alternatives; and greater understanding by physicians and patients of the safety, efficacy, and cost benefits offered by biosimilars.11 Furthermore, the latter two factors are contributing to greater market penetration, with some recently launched biosimilars achieving nearly 70% market share by volume within two years of product launch.14

In fact, a recent FDA study of safety data for patients that did and did not switch to biosimilars showed no statistically significant differences in the number of deaths, non-fatal serious adverse events, and study discontinuations due to adverse events for patients using biosimilars.13 This study provided clear evidence that regulatory approval of biosimilars does ensure they meet the same safety and quality standards required for branded biologics.

According to the Center for Biosimilars, the value of the global market for biosimilars is projected to expand at a compound annual growth rate of 17.6% from $25.1 billion in 2022 to approximately $1.3 trillion by 2032.15 While they have traditionally been developed by large biopharmaceutical firms, an increasing number of startups are a compound developing biosimilar products, including those for more niche markets. This trend may have a secondary impact on outsourcing of biosimilar manufacturing, which in the past has been limited because most large biopharmaceutical firms have preferred inhouse production.

Our parent company, That’s Nice, is committed to supporting the companies and innovators driving the next wave of pharma and biotech innovation. To celebrate That’s Nice’s 30th anniversary, Pharma’s Almanac is diving into 30 groundbreaking advancements, trends, and breakthroughs that have shaped the life sciences, highlighting the industry-defining milestones our agency has had the pleasure of growing alongside. Here’s to 30 years of innovation and the future ahead!

References

“What is a Biosimilar.” U.S. Food and Drug Administration. Accessed 21 Jan. 2025.

“Biosimilar medicines: Overview.” The European Medicines Agency. Accessed 21 Jan. 2025.

Farhat, Fadi et al. “The Concept of Biosimilars: From Characterization to Evolution—A Narrative Review.” Oncologist. 23: 346–352 (2017).

Hofmann, Philipp. “Current Status of Biosimilars and Their Impact on Pharmacovigilance.” Pharmaceutical Executive. 7 Feb. 2024.

Knox, Ryan P, Vineet Desai, and Ameet Sarpatwari. “Biosimilar approval pathways: comparing the roles of five medicines regulators.” Journal of Law and the Biosciences. Jul.-Dec, 2024.

Sheynin, Nicole. “The Booming Market of Biosimilars.” 8 Nov. 2024.

Niazi, Sarfaraz K. “Opinion: A Short History of Biosimilars.” Center for Biosimilars. 27 Feb. 2021.

“Biosimilar Market Report, 4th Edition.” Samsung Bioepis. Q1 2024.

“Biosimilars pipeline report: A guide for understanding the growing market.” AmerisourceBergen. 1 Nov. 2024.

Grimoldi, Veronica. “Navigating the Global Regulatory Landscape for Biosimilars.” Pharma’s Almanac. 16 Jul. 2024.

Jeremias, Skylar. “Biosimilars Account for 23% Market Share, With Wide Uptake Disparities Across Molecules.” Center for Biosimilars. 22 May 2024.

Challener, Cynthia A. “The Opportunities and Challenges Posed by Biosimilar Interchangeability.” Pharma’s Almanac. 7 Mar. 2023.

“FDA, Switching Between Biosimilars and Their Reference Counterparts with Dr. Sarah Yim.” Q&A with FDA Podcast. 8 May 2024.

Alira Health Releases Global Report on Trends and Competitive Dynamics in the Biosimilar Market. Alira Health, 29 Oct. 2024.

Jeremias, Skylar. “Global Biosimilar Market Projected to Reach $1.3 Trillion by 2032.” Center for Biosimilars. 11 Apr. 2024.